Blend Labs ($BLND) Turnaround of a Lifetime

A digital tollbooth on the flow of money between institutions and their customers.

Blend sells software to banks and lenders, who use it to let their customers easily apply for and manage financial products like mortgages, personal loans, and bank accounts online.

I started buying Blend ($BLND) in May 2023 (avg $0.80/share) and still own it. The price today is $3.18/share. In 2 years I think there is a reasonable chance Blend is worth $6/share and potentially a whole lot more.

This is a long post, so I have split it into two parts:

Part 1: I share how I discovered Blend and a few lessons learned.

Part 2: A deep dive investment write up where I explain why Blend’s best days are still in front of them and what Wall Street isn’t appreciating, yet.

Disclaimer: This is not financial advice, I am very clearly biased, no crying in the casino etc.

Part 1: Finding a Diamond in the Mud

July 16, 2021: After 9 years and $665 million in venture funding, Blend Labs ($BLND) went public at $21 a share, good for a $4.4 billion market cap.

March 19, 2023: An anonymous Twitter account, @Dalibali2, unveiled his now-infamous “ShitCo Index”; a basket of 38 VC-backed SPACs and IPOs all taken to the woodshed and down 95-99% from their post Covid ‘21 euphoria highs.

March 20, 2023: I randomly came across the post and immediately drafted a tweet telling Dali exactly where he could stick his index. At that point, I was three years into banging my head against a wall working 80-100 hour weeks trying to get my own venture backed startup to the promised land of product market fit. Regardless of the performance of those stocks, I knew on a visceral level that every single ticker on the “Shitco” index represented the life’s work of a founder who had taken a very real risk to create something out of nothing.

Thankfully, before rage Tweeting at Dali, I came to my senses and realized that he had identified something extraordinarily compelling. The post covid crash of 2022-23 had effectively turned these battered listings into a public-market proxy for late-stage VC. All the companies in his list had some sort of product-market, none of the early stage startup blowup risk, and now anyone could buy these companies for literally a fraction of the total VC funding that had gone into them.

Dali took an equal weighted basket approach to owning all of the companies in his index. So I figured what if I, a startup founder and product builder by day, could go through the same list in my free time and identify individual companies that had legitimate products?

So over the next several weekends I systematically went through the 38 companies in Dali’s index, kicked the tires on the products that these companies were selling and identified three companies (Blend, Carvana and Cardlytics) that I thought had leptokurtic upside.

May 5th, 2023: I realized that while Wall Street had crushed Blend’s share price by 97%, the company had built a best in class platform, expanded its market share from 12% to 20%, grown their unit economics by ~50%, and taken out $100 million in operating costs all during a toughest mortgage industry operating environment of the last 50 years (including the the Great Financial Crisis).

When life presents you with opportunities like this, you have to swing hard and swing big. So I made Blend a 40% position at an average price of $0.80/share ¯\_(ツ)_/¯

June 20th, 2025: Blend is at $3.18 per share, I still own it and I think on a risk-adjusted basis, Blend is more compelling today than it was back then.

Lesson #1: One Man’s Shitco is Another Man’s Treasure

Eighteen months later, the ShitCo Index beat the NASDAQ by more than 80% (see Dali’s follow-up for the numbers). My three picks from the basket; Blend, Carvana, and Cardlytics did meaningfully better.

The point isn’t to take a victory lap, I’m trying to illustrate a core lesson: returns largely flow from the pond you choose to fish in.

For investors: Bombed-out sectors and geographies often have the best asymmetric payoffs. Sidebar: U.S. biotech, the single worst-performing sector of the past three years, looks really interesting to me here. AI has made it easy for anyone with agency, not just domain “experts,” to get up to speed on any topic in the world. You can do the work on individual names if so inclined, or just grab the sector ETF ($XBI) as 2025’s ShitCo proxy.

For founders: Paradoxically, you want to launch in markets where sentiment is max bullish. Raising capital is easier, TAMs are expanding, and customers are open to new solutions. Right now, that market is obviously AI. We are in the first innings of a once in 5 generation opportunity and ignoring AI as a founder (assuming you’ve found a real problem to solve) is just straight up reckless. This is not the time to be a contrarian, run towards the heat!

Lesson #2: One Fish Can Feed the Village

If you can get the pond (market) right, often that single decision alone will literally pull great returns or companies out of you. Don’t believe me? Imagine investing $100 into each of the 38 companies ($3800 total) in the Shitco index on the day the list was published. Now, let’s assume that 37 of the 38 companies in the index went to zero. The remaining 1 company was Carvana at $7 (true story). Today, you’d have $4700 dollars or a 25% return in 2 years, not too shabby.

Lesson #3: Keep A Radically Open Mind

I subsequently exchanged messages with Dali and it turns out that he’s thoughtful and routinely shares great ideas. Go follow him on X if you don’t already!

I’ve been fortunate to interact with some of the world’s sharpest investors in both public and private markets and I’ve noticed a pattern: the best investors always seem to respond to cold DMs/emails and somehow make the time to talk to yahoos like me. I think it is because they don’t judge people on the credentials they come wrapped in; they are constantly underwriting the world for themselves. It is an incredibly exhausting way to approach life, yet the market consistently rewards independent thinkers, so act accordingly.

Part 2: The Investment Case for Blend ($BLND)

Price: $3.18

Fully Diluted Shares: 325M

Market Cap: $1.0B

Cash & Equivalents: $109M

Debt: $0

Enterprise Value: $926M

Target Price & Expected Return: $6 in <2 years, ~100%

What does Blend do and how do they make money?

Banks and lenders use Blend’s software to let their customers easily apply for financial products like mortgages, personal loans and bank accounts online. Each successfully completed transaction triggers a small fee, making Blend a digital tollbooth on the flow of money between institutions and their customers.

Mortgage Suite (~58% of 2025E revenue): Blend earns fees when a loan is funded using its software. They earn about $78 per loan plus ~$15 for related services (income verification etc) which are delivered via 3rd parties operating on Blend’s platform.

Consumer Banking Suite (~34%): Blend earns fees when consumers open or use deposit accounts, personal loans, or HELOCs via the bank’s Blend-powered interface.

Professional Services (~8%): One-time fees for setup, integration, and custom work.

Elevator Pitch In Startup Founder Speak: Blend’s product is awesome, competitors are weak, their founder is a killer and their profits are going to grow a lot when either home prices fall or interest rates come down. Some of the world’s best private equity and hedge funds are buying Blend at these prices. Buy it, forget it and thank me in 5 years.

Elevator Pitch in Hedge Fund Speak:

Platform Transition & Margin Inflection

Blend is converting its mortgage-only franchise into a multi-product banking platform, driving stickier, less-cyclical revenue. As this mix shift accelerates, gross margin, unit economics, and share penetration should all inflect well above current consensus.Setup & Upside

At $3.18 the stock already generates FCF even at trough mortgage volume and carries substantial operating leverage. The trade offers rare “recovery torque” in mortgages plus secular growth from commercial banking; a >2x re-rate inside 24 months is realistic as rates normalize and cross-sell ramps.Forecast Delta vs. Consensus

Street: 75% GM / 14% top-line growth FY-26.

My view: 80% GM / 25–30% growth.

Valuing the consumer-banking segment (45% CAGR, non-cyclical) at a 12x sales (in line with recent acquisition comp) implies you are effectively buying the mortgage franchise at ~3x mid-cycle operating income.Embedded AI Option

Market has yet to price Blend’s data-advantaged position. Owning the top-of-funnel for banks gives first-party data access, enabling a suite of AI products that can materially lift economic value per funded loan (evPFL). Any AI-driven revenue should command a significantly higher multiple on discovery.

Bottom Line: Consensus underestimates both cyclical recovery and structural expansion. The risk-reward skew is attractive; doubling the share price in <24 months is well within base-case parameters.

Ok, I’m intrigued, can you give me more details Rush?

Sure, I was hoping you’d ask. Here’s a deep dive on Blend covering the following topics:

Generational Founder in the Making

Blend’s Distribution Advantage & Platform Moat

Unit Economics: Compelling & Inflecting

Competition

Valuation

Who Else is Buying Blend?

Risks

Generational Founder in the Making

“Never underestimate a man who overestimates himself” - Franklin D Roosevelt

Great companies are forged by exceptional people, and Blend has one in founder-CEO Nima Ghamsari. A Stanford CS grad and early Palantir engineer, Nima owns 5.9% of the company and controls 59% of its voting power.

When I first encountered Blend in early 2023, I almost passed after seeing Nima selling large chunks of his stock near the lows. My knee-jerk reaction was that I didn’t want to own shares of a company where insiders were abandoning ship. A closer look, however, told a very different story. Here’s what was actually going on:

After the IPO, Nima borrowed against his Blend shares to.. Wait for it.. buy even more Blend shares 🤯 The subsequent 70% collapse mortgage volumes drove the share price down, triggered margin covenants forcing him to sell, which in turn drove the price even lower. How did I know this? Because he published an open letter on Blend’s website explaining it to anyone that was paying attention:

“…I increased my personal stake in Blend by borrowing against my existing shares. The sharp decline in fintech valuations triggered loan-to-value covenants that forced me to sell a portion of that collateral… I remain a long-term holder and continue to control the company.”

Most founders use an IPO to (understandably) take some chips off the table. Nima, who literally moonlighted as a semi-professional poker player in college, used his IPO to borrow money to double down. Just pause for a minute here to recognize how insane and rare this is.

Many investors will look at this and think of Nima as reckless. To be fair, Nima did drink too much of the 2021 koolaid. He even signed up for an Elon Musk style options package that incentivized him to 10x Blend’s share price.

So while he did get high on his own supply, dismissing Nima as reckless completely ignores the prior 9 years of great decision making that got Blend to an IPO in the first place. More importantly, this level of self conviction (often erroneously mistaken for arrogance) is exactly what I actively look for in a founder/leader. All courage and no skills just gets you a kamikaze pilot (fun fact: despite all the lore surrounding them, no dive bombing kamikaze pilot ever sunk an Allied fleet carrier, battleship, or cruiser). But when you pair next level confidence with smarts and product building chops which Nima clearly has, you get a relentless founder in it for the long haul worth betting on.

Nima could have very easily abandoned ship. Instead, he stood his ground and painfully rebuilt his company. It is clear to me from interview transcripts that ‘21-23 near death experience has built a resilience into both Nima and the company. TL;DR When smart people with options choose to double down on themselves despite setbacks, pay attention. I think Nima has a point to prove to the world and I’m staying around until he makes it.

As a side note, I also had a brief interaction with Blend’s CFO, Amir Jafari, formerly of ServiceNow, and found both him and the materials produced by his IR team to be impressive.

Blend’s Platform Distribution Advantage

“He who controls the spice controls the universe.” — Baron Vladimir Harkonnen, Dune

A company’s long-term destiny is determined first by its people and second by the quality of its product(s). The financial statements that Wall Street loves to obsess over are lagging indicators of these two things. The good news is that Blend has a best-in-class product and, even more importantly, is now transforming that strength into a durable platform moat.

Why banks need Blend

To understand why Blend has an advantage, it's important to understand why Blend’s customers need solutions like Blend in the first place.

The reason is that most banks and lenders are simply really bad at building software. To fill the gap, they started buying point solutions from various SaaS vendors like Blend. This however led to a spaghetti of systems that no one could fully untangle:

Blend’s misstep and 2023 course-correction

Early fintechs including Blend initially ironically repeated their customers mistake, selling siloed modules. In 2023 Blend rebuilt everything on Blend Builder, a single data and workflow layer that fixes the issues in the table above.

Importantly, Blend’s competitors have NOT truly unified their various offerings into a platform i.e. they are still a hodgepodge of different products that they have acquired at different points in time being held together by duct tape and web hooks underneath the surface, and this gives Blend’s platform a competitive structural advantage.

Tellingly, competitors still rely on acquisitions to introduce new products. To illustrate my point, here is one (of many) examples: when rising rates pushed banks to prioritize capturing deposits, Alkami paid $400m for MANTL. Blend didn’t acquire anyone, they just built an in-house deposits module and pushed it live through Blend Builder making it instantly accessible to all their customers if they wanted it.

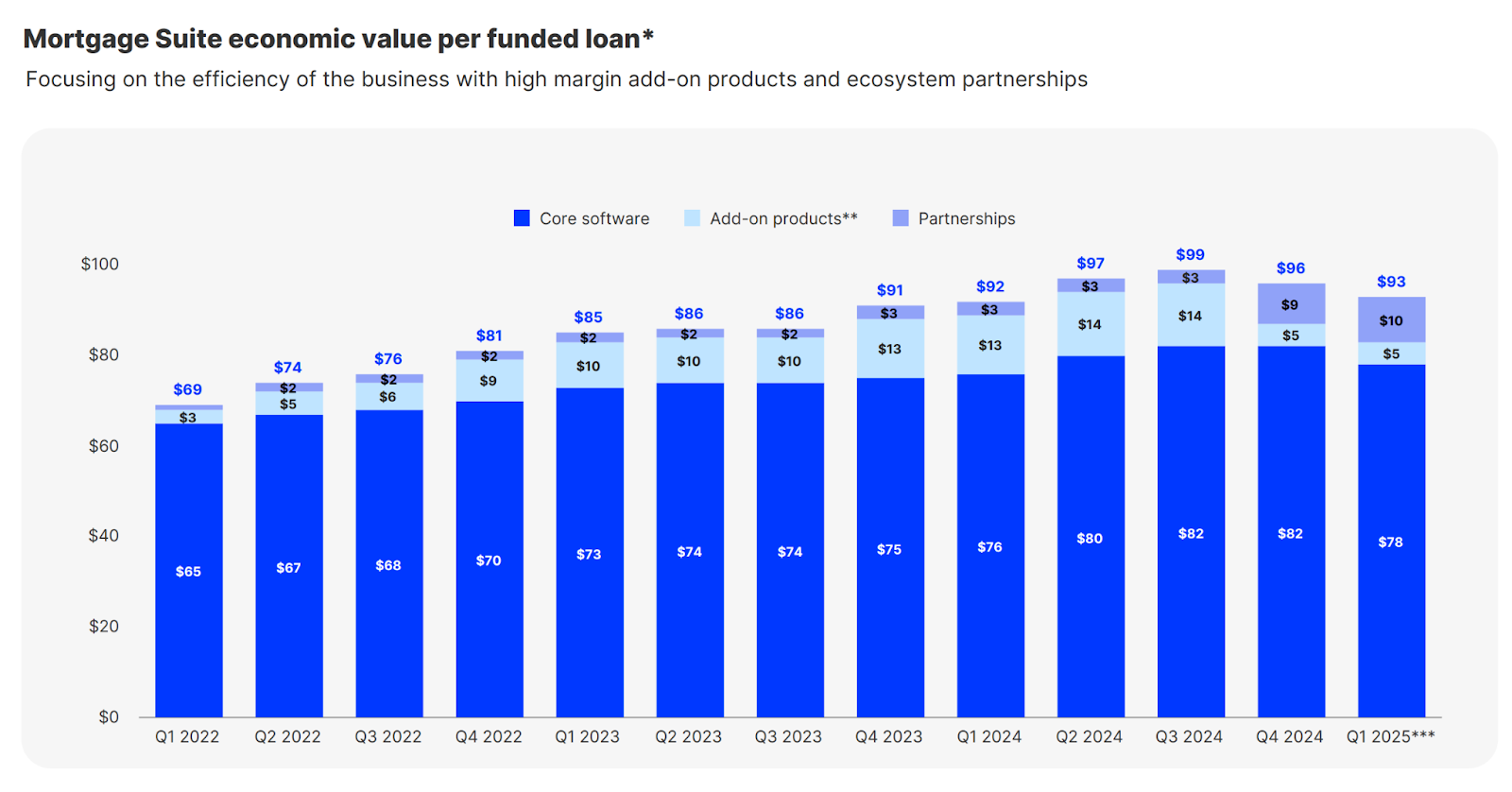

Result: Blend has been able to grow their economic value Per Funded Loan (evPFL) from $69 in Q1 2022 to $99 in Q3 2024, a 43% increase in the face of a 70% decline in mortgage volumes, a heroic achievement. They were able to do this because they are leveraging their entrenched distribution into financial institutions and selling new products via Blend Builder.

Per Nima’s comments on the Q1 2025 conference call, Blend’s largest customers who are using all their products are already at an evPFL of $170. Intriguingly, the evPFL today is a tiny fraction of the total cost of originating a mortgage ($10,697). Translation: Blend is undermonetizing their product today and their customers aren’t going to mind too much if Blend raises prices in the future, an excellent position to be in as a business.

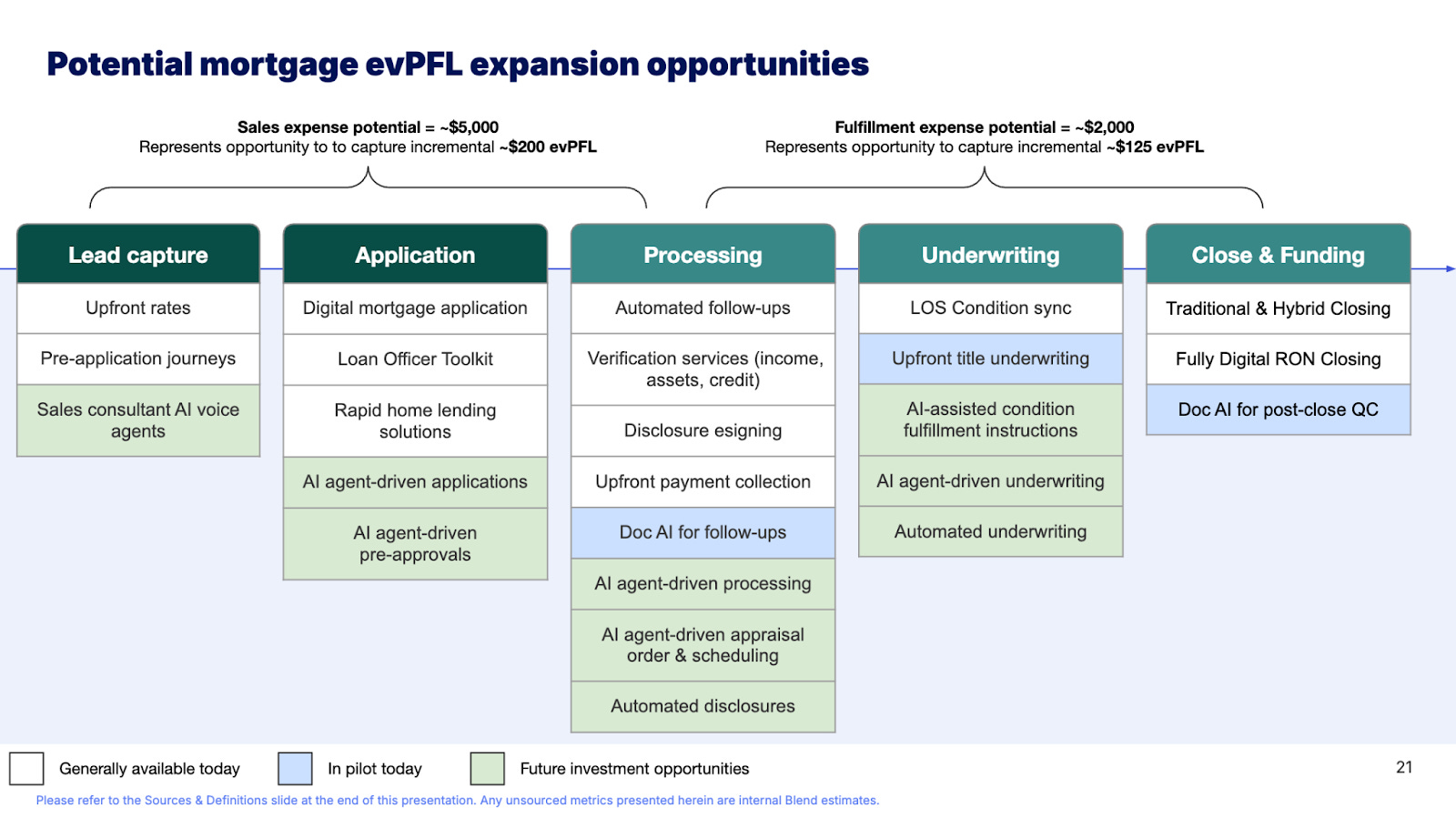

Lastly, Blend put out a roadmap (below) for their product expansion plans which showed a path to an incremental $325 in evPFL. Most excitingly, they have designs on expanding into the Sales and Fulfillment piece of the origination process which is much juicier. I think they are being conservative with the $325 estimate because if they are able to deliver on even half of what is being promised on this roadmap, they will capture a lot more given the nature of the products they are moving into. This does however put them on an eventual collision course with the 800 pound gorilla ICE (they own Encompass) who are currently mostly downstream of Blend, so it’s something to keep an eye on.

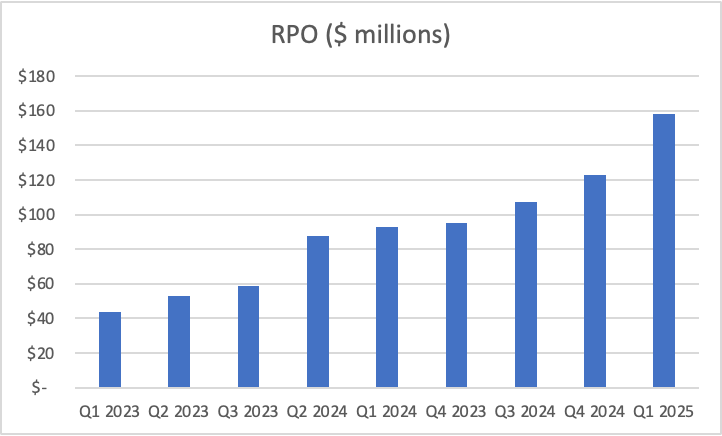

Their consumer banking business? Same story. Most investors didn’t even take this segment seriously 2 years ago, and now it is a $45M ARR run rate business growing at a 45% CAGR. Here are their RPO numbers, which tell the same story: Blend’s platform is gathering steam.

Notably, their RPO target for 2025 was $150M and they ended up exceeding it in Q1 2025.

Unit Economics

“If the unit economics don’t work, the business can’t work” - Fred Wilson, USV

Blend doesn’t give us the split in unit economics of their two businesses: mortgage and consumer banking but we can try to estimate it.

Mortgage suite: We know that in Q1 2025 Blend earned an evPFL of $93. This number has been declining for the past 2 quarters because of a mix shift towards smaller customers (independent mortgage banks) and new customers onboarded into the platform who are still ramping up.

Historically Blend provided add-on services like KYC, verifications, insurance, etc. in-house, eating data-provider fees and support costs that suppressed contribution margins. They are now flipping that model: they are plugging trusted third-party vendors into the platform, letting those partners run the heavy ops, and keeping a software-like take-rate on every transaction. As the mix shifts from owned services to partner-delivered services, each incremental dollar flows through at near-pure gross profit.

My variant perception on mortgage gross margins: By keeping core-software margins at ~77% and lifting third-party services to 90% while they represent roughly 16% of mix, the Mortgage Suite’s blended gross margin rises to ~80% (0.84 × 77% + 0.16 × 90% ≈ 79%).

The gross margins on the Consumer Banking suite are more straightforward. The combined software platform runs ~79% gross margin, and the legacy Mortgage Suite (still 66% of software revenue) is at ~75–77%. Plugging in the numbers therefore puts the Consumer Banking Suite at roughly 84–87% gross margin today.

Putting the two together, I model 80-82% gross margins vs the street who are still modeling 75% gross margins even into 2026.

Operating expenses Blend gives us (below) of ~65% in 2025 which I reckon will go to 60% by 2026. This leaves us with a 20-25% Operating Profit Margin.

The most important takeaway: Blend is transitioning away from their service heavy business model and essentially now operating an App Store where third party providers operate on Blend’s rails to provide banks and lenders services like income verification, title insurance etc. This business model shift will result in Blend’s gross margins inflecting higher and the company operationally more focused on building great software. The App Store model is incredibly powerful and starts forming a real compounding moat for Blend; just as the App Store has served as a moat for Apple, Google, Shopify and Salesforce. TL;DR Blend is in excellent company and on the right path.

Competition

Mortgage Suite: Blend’s only credible rival IMO is SimpleNexus, which is owned by nCino. My tire kicking led me to the conclusion that SimpleNexus lags Blend in functionality, and Nima Ghamsari has noted for two consecutive quarters that Blend is the sole vendor appearing on bank RFP short-lists. It’s revealing that, even though nCino and Blend share several major customers (with nCino serving their consumer needs and Blend mortgage), as far as I can tell by cross referencing logos using the Wayback machine, SimpleNexus was unable to coax any of those clients onto its platform, even when Blend was on the brink of bankruptcy. Roostify has languished inside CoreLogic, while ICE’s Encompass sits farther downstream. The bigger threat IMO comes from Rocket and United Wholesale Mortgage, which compete directly with Blend’s bank customers for origination share. But with only ~40% of U.S. mortgages completed online, the addressable runway remains massive for everyone.

Consumer Banking Suite: This market is more crowded: nCino, Alkami, Q2, and others are active and have competitive products, but Blend’s suite is outpacing its own targets. Lenders appear drawn to Builder’s one-platform delivery of both mortgage and consumer-banking products, giving Blend a differentiated edge even in a competitive field.

Valuation

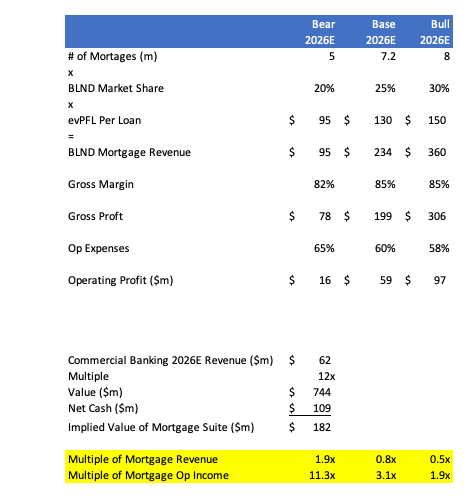

Blend’s Consumer Suite is expected to make $62M ARR in 2026 and be growing at ~35%. MANTL was just acquired by Alkami for $400M for 13x 2025E revenues which are growing at 30%. Using this as a comp, we can use a 12x multiple for Blend’s consumer business and estimate it will be worth $744M in 2026.

Estimating the value of the Mortgage Suite is trickier because revenues are highly dependent on mortgage volumes (which are inversely tied to rates). Given that we appear to be at the peak of the rates cycle and there is considerable political pressure to reduce interest rates, and there is a ton of pent up demand for re-finances, it’s not crazy to think that mortgage volumes will go back to ~7.2M by 2026 which is the 20 year historical median mortgage volume. Blend currently has a ~20% market share, I think it is fair to assume they’ll be at 25% by 2026. Blend currently makes $93 per funded loan. They’ve introduced a whole bunch of new products and existing current cohorts of customers will mature, so it’s not crazy to think evPFL will be $130 by 2026. Putting it all together:

Essentially at $3.18/share today you’re buying Blend’s best in class mortgage platform for 3x next year’s estimated operating income. For context, autos which are also cyclical trade and less profitable trade at 16x operating income on average.

If we assume the mortgage business is worth 5x EV/Sales or 20x Operating Income, the stock doubles.

Bonus: Blend invested $2.5M in Bilt’s seed round at a $60M valuation. It looks like Bilt is on their way to being a decacorn (last valuation of $3.25B), so we could see a return on this hidden asset on their balance sheet in the future if Bilt goes public or gets acquired.

7/11/2025 Update: Turns out Blend invested in Bilt at a $350M valuation not $60M. I erroneously got the $60M number from a press article that misconstrued the round size ($60M) for the valuation ($350M). Bilt also announced a private round of funding on 7/10/2025 at a $10.75B valuation.

Who Else is Buying Blend?

“Oh my God, it’s like we’re sharing a brain!” — Alexis Rose, Schitt’s Creek S02 E02

While it is important to do independent work and reach your own conclusions in investing, it’s good to know other (much smarter) investors have also converged on Blend seeing the opportunity.

Brian Sheth’s (formerly President of Vista Equity Partners) new fund Haveli Investments invested $150M in Blend via preferred that convert at $3.25/share and Brian sits on Blend’s Board. Extraordinarily thoughtful and high conviction public markets investor Dennis Hong of Shawspring has been adding to his BLND position per their latest 13-F filing. Joe Lonsdale, cofounder of Palantir and seed investor in Blend through 8VC took the unusual step of publishing a public letter defending Blend. Lightspeed, another early investor, remains fully invested in the company. Peter Thiel led their Series C. Last but not the least, the company was buying back (small amounts) of their own shares in the open market at $3.30/share this past quarter.

Risks

“Trust Allah, but tie the camel” - Arab proverb

Rates stay flat or go higher: Blnd’s destiny for better or worse is tied to interest rates that are outside of their control. In a world in which rates go higher, the Blend re-rating story will get delayed.

Mitigant: I think we’re at the point where higher rates will cause a meaningful home price correction, making homes more affordable offsetting some of the demand destruction. If you want to get fancy (I never get fancy), you could hedge out your rates exposure via derivatives.

Capital allocation: Blend made a disastrous acquisition of Title365 from Mr. Cooper in 2021. They paid $450M for it and just recently sold it off to Covius for an undisclosed sum (wouldn’t surprise me if they gave it away for free). Past shareholders have paid the price for this acquisition and the goodwill’s already been written off, but another bad acquisition will sink the company.

Mitigant: With Dennis Hong and Brian Sheth at the table and a new CFO (ex ServiceNow) in place, I don’t think there is a high probability of this happening.

As alluded to in the competition section, both Rocket and UWMC are making massive investments in technology. They compete directly with Blend’s customers so there is a chance that they start taking share from banks and lenders on an accelerated basis.

Mitigant: Only 40% of mortgages are currently done digitally. There is a strong structural tailwind of digitization that is greater than any share loss. Further, Blend will continue to win new customers offsetting any share loss.

Feels a bit silly to send out an investment idea the same weekend stealth bombers are dropping bunker buster bombs on nuclear research facilities, so I’ll just say it: if oil spikes up leading to sticky inflation or a nuke is launched, we’re in trouble.

Mitigant: In the long run this should be noise but if it isn’t we’ll have bigger problems to worry about.

If you’ve made it to the end, I’d welcome your feedback and/or pushback on this write up.

Stay curious,

Rush

This was an awesome read, thanks.

Am I understanding correctly? In your bear case you have both evPFL and operating profit margins *much* higher than what they are guiding to for 2025.

I suppose I can see evPFL getting back to the $90s for 2026, but what gives you confidence that they can reach 35% operating margin in 26 when they're nowhere close to that today?